The second tranche of the JobKeeper scheme changes the eligibility test for employers and the method and amount paid to employees.

If your business currently receives JobKeeper, your arrangements will generally remain unchanged until 27 September 2020. From 28 September 2020, employers seeking to claim JobKeeper payments will need to reassess their eligibility and prove an actual decline in turnover.

Eligibility

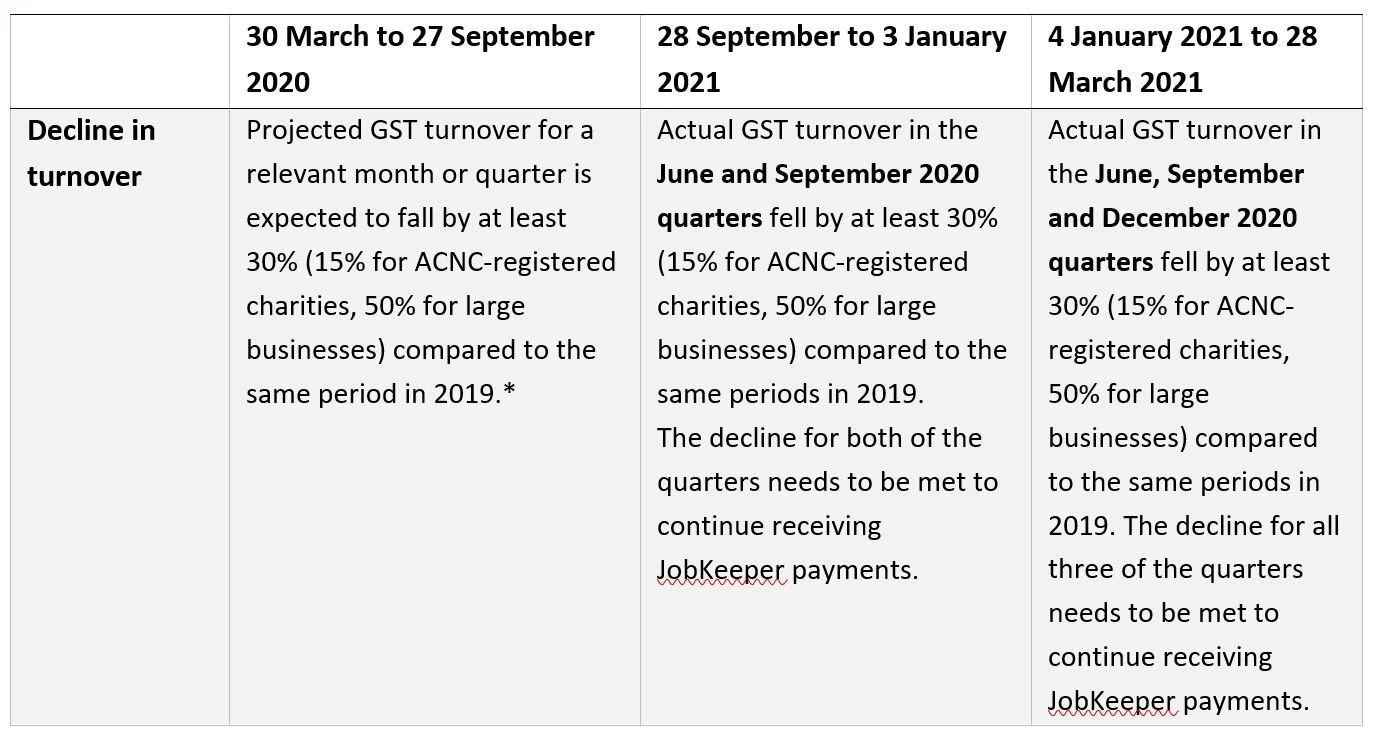

To continue receiving JobKeeper payments, employers will need to reassess their eligibility with reference to actual GST turnover for the June and September 2020 quarters (for payments between 28 September to 3 January 2021), and again for the June, September and December 2020 quarters (for payments between 4 January 2021 to 28 March 2021).

Eligible employers

The broad eligibility tests to access JobKeeper remain the same with an extended decline in turnover test.

On 1 March 2020, carried on a business in Australia or was a non‑profit body pursuing its objectives principally in Australia; and

before the end of the JobKeeper fortnight, it met the decline in turnover test*:

>15% for an ACNC-registered charity (excluding universities, or schools within the meaning of the GST Act – these entities need to meet the basic turnover test)

> 50% for large businesses:

aggregated turnover for the test period is likely to be $1 billion or more, or aggregated turnover for the previous year to the test period was $1 billion or more (a small business that forms part of a group that is a large business must have a >50% decline in turnover to satisfy the test).

>30% for all other qualifying entities.

And, was not:

on 1 March 2020, subject to Major Bank Levy for any quarter ending before this date, a member of a consolidated group and another member of the group had been subject to the levy; or

a government body of a particular kind, or a wholly-owned entity of such a body; or

at any time in the fortnight, a provisional liquidator or liquidator has been appointed to the business or a trustee in bankruptcy had been appointed to the individual’s property.

1 March 2020 is an absolute date. An employer that had ceased trading, commenced after 1 March 2020, or was not pursuing its objectives in Australia at that date, is not eligible.

*Additional tests apply from 28 September 2020.

Additional decline in turnover tests

To receive JobKeeper payments from 28 September 2020, businesses will need to meet the basic eligibility tests and an extended decline in turnover test based on actual GST turnover.

* Alternative tests potentially apply where a business fails the basic test and does not have a relevant comparison period.

Most businesses will generally use their Business Activity Statement (BAS) reporting to assess eligibility. However, as the BAS deadlines are generally not due until the month after the end of the quarter, eligibility for JobKeeper will need to be assessed in advance of the BAS reporting deadlines to meet the wage condition for eligible employees. However, the ATO will have discretion to extend the time an entity has to pay employees in order to meet the wage condition.

Alternative arrangements are expected to be put in place for businesses and not-for-profits that are not required to lodge a BAS (for example, if the entity is a member of a GST group).

Alternative tests

The Commissioner of Taxation will have discretion to set out alternative tests that would establish eligibility in specific circumstances where it is not appropriate to compare actual turnover in a quarter in 2020 with actual turnover in a quarter in 2019, in line with the Commissioner’s existing discretion.

Eligible employees

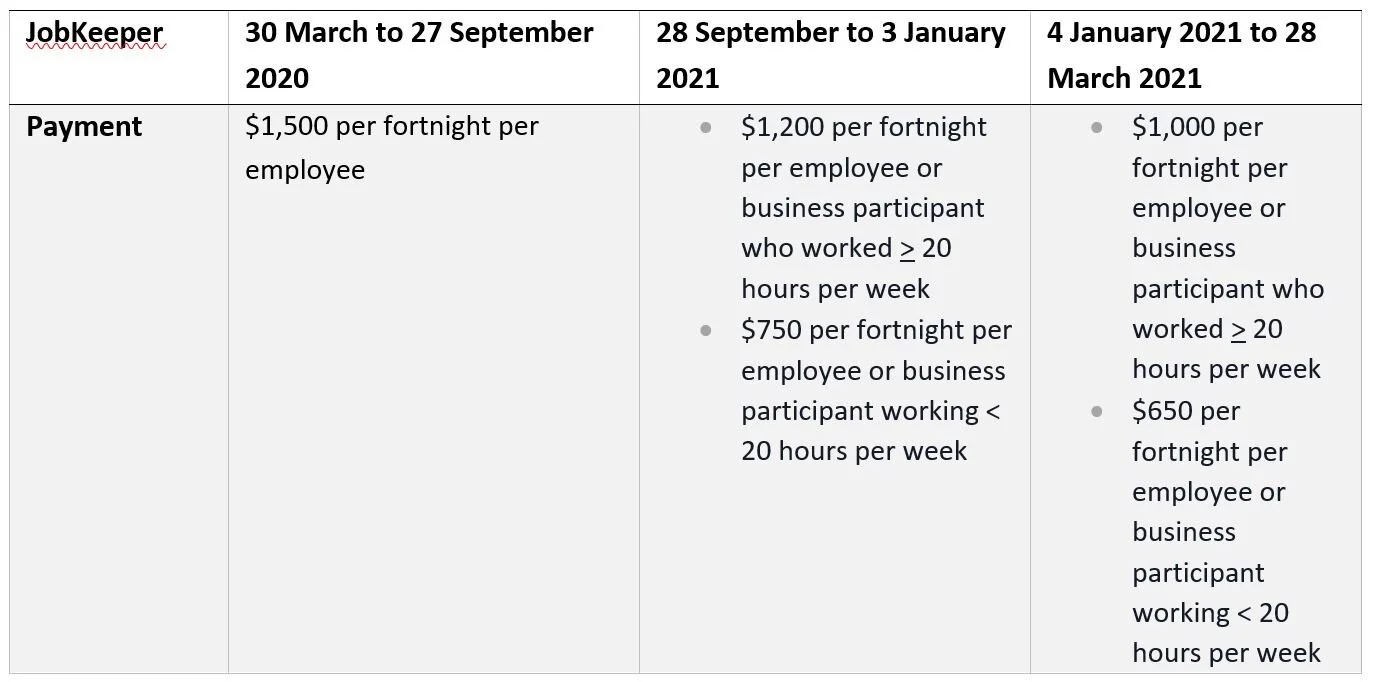

Employee eligibility will remain broadly the same but the value of the payment will change from 28 September based on average weekly hours in February 2020.

On 1 March 2020:

Was aged 16 years and over; and

If the individual was aged 16 or 17, was either financially independent or was not undertaking full-time study;

Was an employee other than a casual, or was a long-term casual*; and

Was an Australian resident (under the meaning of the Social Security Act 1991), or a resident for tax purposes and held a Subclass 444 (Special category) visa**.

And, at any point during the JobKeeper fortnight:

Was an employee of the employer; and

Was not an excluded employee:

An employee receiving parental leave pay or dad and partner pay; or

An employee receiving workers compensation payments in relation to total incapacity.

And, has provided the JobKeeper Payment Employee Nomination to the employer:

Agreeing to be nominated by the employer as an eligible employee under the JobKeeper scheme; and

Confirming that they have not agreed to be nominated by another employer; and

If they are a long-term casual, they do not have permanent employment with another employer.

*A ‘long term casual employee’ is a person who has been employed by the business on a regular and systematic basis during the period of 12 months that ended on 1 March 2020 (1 March 2019 to 1 March 2020). These are likely to be employees with a recurring work schedule or a reasonable expectation of ongoing work.

JobKeeper payments

Assessing if an employee has worked 20 hours or more

JobKeeper payments from 28 September 2020 are paid at a lower rate for employees who worked less than 20 hours per week on average in the four weeks of pay periods before 1 March 2020.

The Commissioner of Taxation will have discretion to set out alternative tests for those situations where an employee’s or business participant’s hours were not usual during February 2020. Also, the ATO will provide guidance on how this will be dealt with when pay periods are not weekly.

Can I keep getting JobKeeper until September?

If your business and your employees passed the original eligibility tests to access JobKeeper, and you have fulfilled your wage requirements, you can continue to claim JobKeeper up until the last JobKeeper fortnight that ends on 27 September 2020.

ATO assistant commissioner Andrew Watson said in a recent interview, “Once you’re in, you’re in to the end of September. If you meet the eligibility test once, you’re in it for the whole time.” The original eligibility test was a once only test although there are ongoing conditions that need to be satisfied for each JobKeeper fortnight.

Please contact us if you have any questions.

**Information supplied with thanks to Knowledge Shop